How Private Markets Work: An Investor’s Guide to Understanding and Investing in Alternative Assets

Learn how private markets work—from private equity to real assets. Discover how they differ from public markets, what risks they carry, and how investors can access them today.

For much of modern financial history, capital markets have been viewed through a binary lens: public or private. Public markets—transparent and highly liquid—enable continuous trading of equities and bonds on regulated exchanges. Private markets, by contrast, operate outside public view, governed by bespoke contracts, lower transparency, and substantially different risk and return drivers.

Until recently, private markets were dominated by institutions and high-net-worth individuals. Today, broader access and greater interest in diversification are reshaping this landscape. Understanding private markets is now a prerequisite for informed portfolio management, not simply a specialist concern.

This guide presents a structured, analytical overview of how private markets function, how they distinguish themselves from public markets, and what investors should know before considering an allocation to this segment of the global capital markets.

What Are Private Markets? (In Plain Terms)

Private markets comprise investments in assets not listed on public exchanges. This includes ownership in private companies, direct participation in real estate or infrastructure, or lending capital outside established bond markets.

In public markets, shares of a company become available to the broad investing public through a listing process. Private markets cover all transactions prior to that point, as well as assets that may never be listed.

The Key Difference: Access and Transparency

- Public markets are accessible, highly regulated, and priced in real time.

- Private markets are accessed via negotiated transactions, are considerably less liquid, and operate within a framework of private agreements rather than universal public oversight.

Public markets function like a standardized retail environment: transparent pricing and easy access. Private markets are analogous to engaging a specialist for a tailored solution—negotiation, customization, and extended process timelines are standard.

Core Characteristics of Private Markets

A grounded understanding of private markets' operational fundamentals is essential for any well-informed allocation decision.

1. Illiquidity (The Lock-Up Period)

Private market investments typically entail a multi-year commitment—often five to ten years—during which capital cannot be readily accessed or withdrawn.

While this illiquidity may initially seem limiting, it allows investment managers to execute long-term value creation strategies without the constraints of short-term redemption pressures. This alignment of interests is a principal rationale for private market structures.

2. Valuation Frequency

Unlike public markets, where valuations are observable at any moment, private assets are subject to periodic valuation—most commonly quarterly or annually—using structured models, peer comparisons, and independent appraisals.

This systematic but less frequent process results in lower observable volatility ("valuation smoothness") but places significant emphasis on robust methodology and managerial transparency.

3. Longer Investment Horizons

Private investments demand a patient capital approach. Realization of returns is usually contingent on outcome-driven events—such as corporate sales or initial public offerings—materializing over an extended period.

For capital intended for near-term liquidity, private assets are generally not appropriate. The time horizon aligns capital with measured value creation, not reactive price movement.

The Main Types of Private Market Investments

Private markets are a collection of asset classes, each offering distinct attributes for portfolio construction.

1. Private Equity (PE)

Private equity encompasses investment in privately held companies, ranging from early-stage innovation (venture capital) to mature enterprise transformations (buyouts).

- Venture Capital (VC): Targeted at high-potential, early-stage companies—risk and return expectations are elevated.

- Growth Equity: Allocated to established businesses seeking capital for expansion or evolution.

- Buyouts: Acquisition and operational improvement of mature companies with a focus on long-term value capture.

Strategic intent: Achieve capital appreciation via business restructuring and strategic operational change.

2. Private Credit

Private credit refers to the provision of debt capital directly to private entities, bypassing traditional public debt markets.

- Delivers recurring income through contractual interest.

- Typically exhibits lower risk than equity, though with capped upside.

- Representative forms include senior secured lending, mezzanine finance, and distressed credit.

Objective: Secure predictable yield and diversify exposures beyond traditional fixed income.

3. Real Assets

Investment in tangible, productive assets functions as a stabilizing component in diversified portfolios:

- Real Estate: Direct ownership of income-generating properties can balance capital appreciation and steady cash flow.

- Infrastructure: Long-duration assets—such as energy networks, transportation links, and digital infrastructure—often feature inflation protection and multiyear visibility.

These investments are well positioned as hedges against inflation and sources of contractual cash flow.

How Private Markets Create Returns (and Risks)

The rationale for private market investing is rooted in the illiquidity premium—the additional compensation investors seek for accepting structural barriers to liquidity and increased complexity.

The Return Profile

Empirical studies indicate that, over extended periods, upper-tier private equity and venture funds have outperformed public benchmarks. However, performance is highly dispersed:

- Top-decile funds may substantially multiply invested capital.

- Lower-quartile funds frequently underperform, sometimes failing to return principal.

Manager selection and privileged access to high-quality investments are fundamental to achieving favorable outcomes.

The Risk Profile

Risk assessment in the private domain departs from the volatility-driven frameworks applied to listed assets. Key risks include:

- Liquidity Risk: The inability to re-access capital prior to predefined exit events.

- Execution Risk: Failure to implement business or asset-specific growth strategies.

- Transparency Risk: Reduced frequency and granularity of performance data.

Private asset returns tend to exhibit lower correlation with public valuations, contributing to diversification but emphasizing the need for in-depth diligence.

Why Private Markets Require a Different Portfolio Approach

Optimization of private allocations demands specific portfolio frameworks acknowledging unique risk, liquidity, and operational characteristics.

1. The J-Curve Effect

Returns in private markets are commonly negative in initial periods, reflecting costs and delayed revenue realization, then turn positive as assets mature ("the J-Curve"):

- Early commitments result in net outflows and unrealized losses.

- Value accretion and exits in mid-to-late periods transition results to positive territory.

2. Diversification by Vintage Year

Given the unpredictability of market cycles, investors frequently stagger commitments across multiple 'vintage years'. This temporal diversification limits the risk associated with investing predominantly at a single point in the cycle.

3. Balancing Liquidity and Access

Prudent allocation to private assets must be paired with sufficient liquid resources to ensure ongoing financial flexibility.

A portfolio should integrate carefully calibrated private market exposure (commonly 10–30%), adjusted according to liquidity requirements and investment objectives.

The Growing Accessibility of Private Markets

Structural barriers to private markets are diminishing:

- Digital investment platforms enable a broader set of accredited investors to participate.

- Tokenization and fractional investment models lower minimum entry requirements.

- Evolving regulation expands potential access while requiring persistent diligence.

The resulting democratization increases opportunity but also necessitates disciplined, evidence-based evaluation of new access points.

How to Get Started in Private Market Investing

A methodical approach is vital for new entrants:

- Define Objectives: Clarify return targets and the role of private markets within your overall strategy.

- Assess Liquidity Needs: Reserve sufficient liquid assets for planned and unforeseen expenses.

- Research Access Platforms: Select intermediaries with demonstrated accountability and track record transparency.

- Start Small and Diversify: Allocate gradually, diversify by investment year and sector, and monitor outcomes.

- Leverage Technology: Employ comprehensive portfolio tools such as Findex for consolidated asset monitoring and reporting.

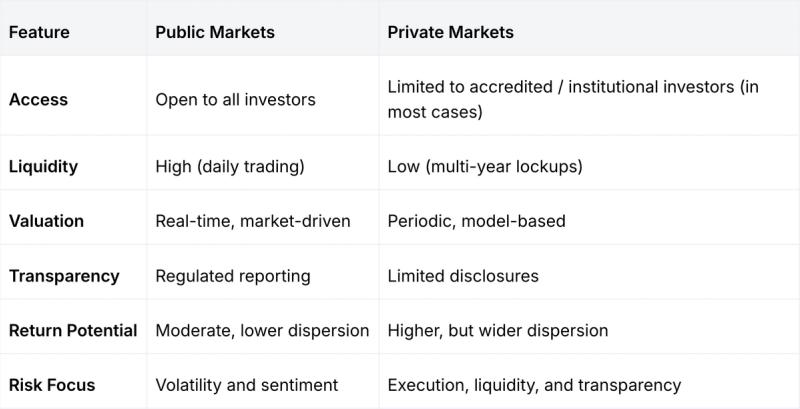

Private Markets vs. Public Markets: A Quick Comparison

Why Visibility and Technology Now Matter Most

Comprehensive reporting and infrastructure are now central to efficient private market investing.

Fragmented data across multiple investment accounts poses a challenge for assessing total exposure, liquidity, and performance.

- Accurate portfolio monitoring depends on unified visibility.

- Real-time reporting supports efficient risk and liquidity management.

- Integrated digital platforms such as Findex provide institutional-level monitoring—enabling precise tracking of both public and private assets for improved decision-making.

👉 Explore Capital Opportunities on MyFindex and centralize your investment oversight.

Frequently Asked Questions (FAQs)

1. What qualifies as a private market investment?

Any investment not traded on public exchanges—such as private equity, venture capital, real estate, or private credit.

2. Are private markets riskier than public markets?

They carry different risks—especially illiquidity and limited transparency—but can offer higher long-term returns if managed correctly.

3. How can individual investors access private markets?

Through regulated private market platforms, feeder funds, or digital investment managers offering fractional access.

4. What is the illiquidity premium?

The extra return investors demand for tying up capital long-term in exchange for reduced liquidity.

5. How much should I allocate to private markets?

For most diversified portfolios, 10–30% allocation is typical, adjusted based on liquidity needs and experience.

6. How can technology help in private market investing?

Platforms like Findex automate tracking, valuation, and reporting—bridging the gap between public and private assets.

Keep reading

Related guides

How Do I Access Private Market Investments as an Individual Investor?

Access to private markets is more available than ever, but management requires precision. Compare access strategies, understand persistent barriers, and learn to track and oversee private assets effectively.

What Are the Risks of Private Market Investments? A Guide for Modern Investors

Private market investing offers unique opportunities but requires disciplined oversight. Learn to manage illiquidity, valuation lag, and reporting complexity with the right tools.

How to Start Investing in Stocks with Confidence

Learn how to invest in stocks as a beginner with our comprehensive guide. We'll walk you through the practical steps and psychological considerations for investment success.

Your complete net worth, finally in one place.

Join investors using Findex to consolidate, track, and grow their portfolios. One view of everything you own.

No payment information required.